Medical Tourism Market 摘要

2025年全球医疗旅游市场规模预计为5824.8万美元,预计到2035年将达到2928.661亿美元,2025年至2035年复合年增长率为18.2%。主要增长动力包括发展中国家的低成本治疗、先进的手术、现代化的医院、熟练的医生、改善的连通性和个性化的患者护理。

医疗保健成本差距的扩大以及人们对国外负担得起的高质量治疗的认识不断提高,正在推动医疗旅游业的增长。患者更喜欢在改善的出行便利、数字医疗平台和国际医院认证系统的支持下进行手术、生育和健康服务的跨境护理。

世卫组织全球健康数据集显示,每年超过 13 亿次国际游客流动支持跨境医疗保健的可及性,而斯坦福 AIMI 等先进的人工智能健康数据系统显示,60 多个国家越来越多地采用数字诊断,提高了医疗旅行决策的治疗信心和患者流动性。

主要市场趋势和亮点

在富裕国家不断上涨的医疗保健成本、数字工具以及患者对国外高质量、负担得起的个性化护理的需求的推动下,医疗旅游市场正在快速发展。

- 由于全球对选择性国际美容手术的高需求,到 2024 年,整容手术将占据 28% 的市场份额。

- 私人医疗保健占据主导地位,占 72% 的份额,提供先进的基础设施、优质服务和强大的国际患者管理系统。

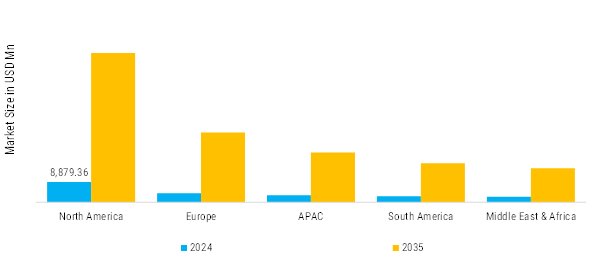

- 受高昂的医疗成本和跨境治疗需求的推动,北美地区贡献了全球 45% 以上的收入。

- 受漫长的等候名单和跨境医疗服务的推动,2024 年欧洲的价值为 147.8387 亿美元,占据 30% 的份额。

市场规模与预测

| 2024 年市场规模 | 49,279.57 (USD Million) |

| 2035年市场规模 | 2,92,866.10 (USD Million) |

| CAGR (2025 - 2035) | 18.2% |