Whole Slide Imaging Market Summary

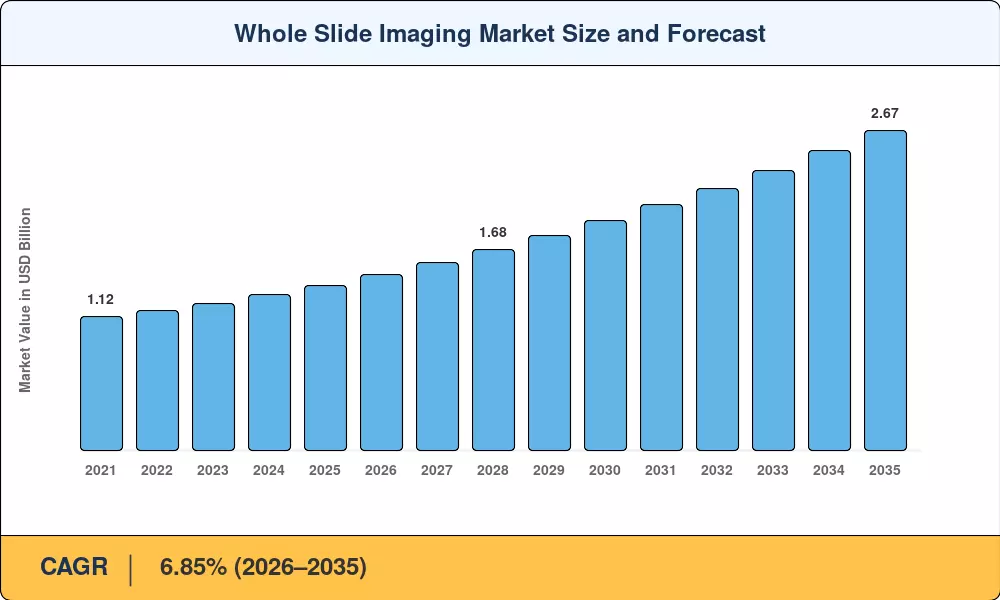

The Global Whole Slide Imaging Market size was valued at USD 1.38 Billion in 2025, and the market is projected to grow from USD 1.47 Billion in 2026 to USD 2.67 Billion by 2035, registering a CAGR of 6.85% during the forecast period 2026–2035. Two structural catalysts underpin the trajectory: the U.S. FDA's broadening 510(k) clearance pathway for digital pathology scanning devices, and cumulative hospital IT modernization budgets exceeding USD 48 Billion globally during 2024–2028 [1]. As reimbursement frameworks catch up with technology, capital-expenditure hesitation among mid-tier laboratories is dissolving.

A generation of glass-slide-only workflows is giving way to fully digitized histology slide digitization pipelines. Legacy manual microscopy, which still dominates roughly 60% of diagnostic pathology volume worldwide, is being displaced by high-throughput scanners capable of producing 40× whole-slide images in under 60 seconds. The European Commission's €2.1 Billion digital health action plan (2024–2027) explicitly earmarks funding for virtual microscopy systems in cross-border tumor-board consultations [2]. AI-assisted tissue analysis algorithms layered atop these platforms have already demonstrated 4–7% improvements in diagnostic concordance for breast cancer grading [3].

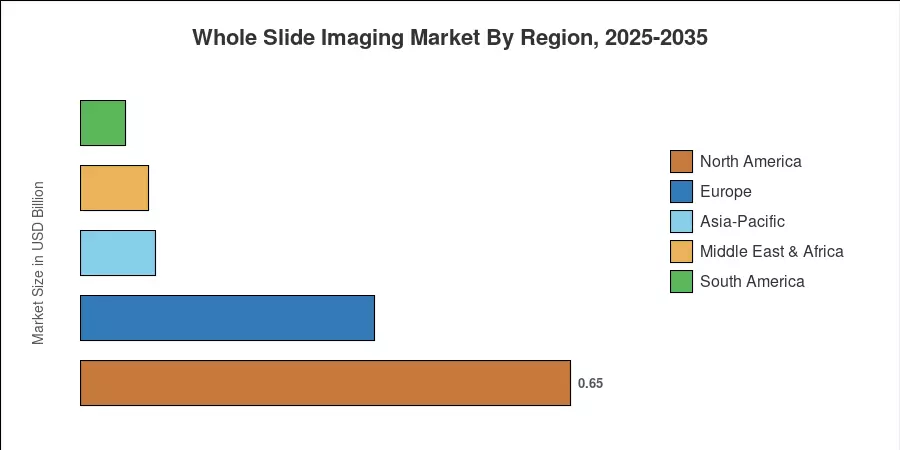

North America commanded approximately 46.8% of the whole slide imaging market in 2025, buoyed by early regulatory clarity and dense academic medical-center networks. Asia-Pacific registers the fastest CAGR at 7.58% through 2035, driven by China's "Healthy China 2030" digital diagnostics mandate and India's National Digital Health Mission. Europe holds the second-largest share at roughly 28%, anchored by the UK's National Health Service pathology network consolidation program. As telepathology diagnostic tools scale across emerging economies, the whole slide imaging market is positioned for a decade of compounding digital adoption.

Key Report Takeaways

• By Component

- Hardware accounted for 68.7% of the whole slide imaging market share in 2025, reflecting continued high-throughput scanner procurement cycles across hospital networks

- Software platforms are expanding at a 7.15% CAGR through 2035, driven by cloud-based image-management suites and AI-assisted tissue analysis plug-ins

• By Scanner Type

- Brightfield scanners held 55.5% share of the whole slide imaging market in 2025, serving as the workhorse for routine hematoxylin-and-eosin histology slide digitization

- Fluorescence scanners are advancing at a 7.48% CAGR to 2035, propelled by rising immunofluorescence and multiplex-assay workloads

• By Application

- Telepathology captured 40.3% of the whole slide imaging market in 2025, reflecting the surge in remote diagnostic consultations post-pandemic

- Immunohistochemistry is the fastest-growing application segment at 7.84% CAGR through 2035

• By Region

- North America anchored 46.8% share of the whole slide imaging market in 2025, while Asia-Pacific registers the strongest growth trajectory at 7.58% CAGR

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology integrates bottom-up revenue modeling from scanner shipments, software-license revenues, and service contracts across 32 countries, triangulated against top-down macro indicators including healthcare IT capital expenditure and pathology-procedure volumes.

.webp?v=1782120685)