Fiber Optic Test Equipment Market Summary

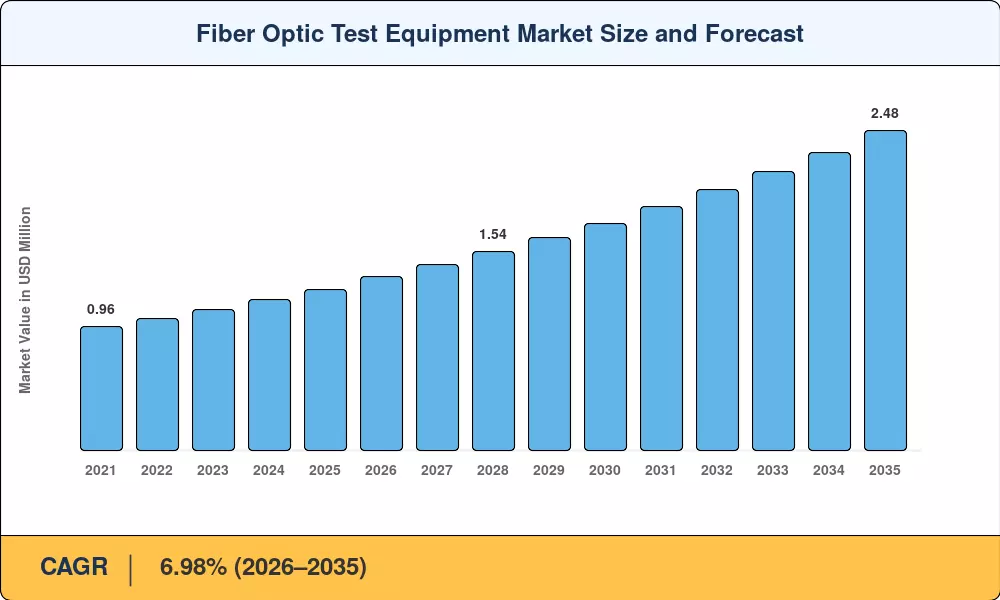

The fiber optic test equipment market stood at USD 1.25 billion in 2025 and is projected to reach USD 1.35 billion in 2026 before climbing to USD 2.48 billion by 2035, registering a CAGR of 6.98% across the forecast window. Two forces anchor this expansion: the global push toward 5G network densification—where fronthaul fiber runs require rigorous optical fiber testing tools for every splice and connector—and a wave of government-backed rural broadband initiatives, including the U.S. BEAD program's USD 42.45 billion allocation, that mandate stringent fiber cable certification equipment protocols before network acceptance [2][3].

The technology transformation is changing the way operators check connection integrity. AI-enabled OTDR fiber measurement platforms that can diagnose errors in less than 90 seconds and send the data to centralized network-orchestration dashboards are replacing legacy copper-centric testers. Hyperscale data center operators moving to 800 G coherent optics are now requesting optical power meter instruments calibrated for wideband C+L configurations, a capability that scarcely existed three years ago [4]. The top five suppliers have invested more than USD 320 million a year in test devices for next-gen fiber networks [5].

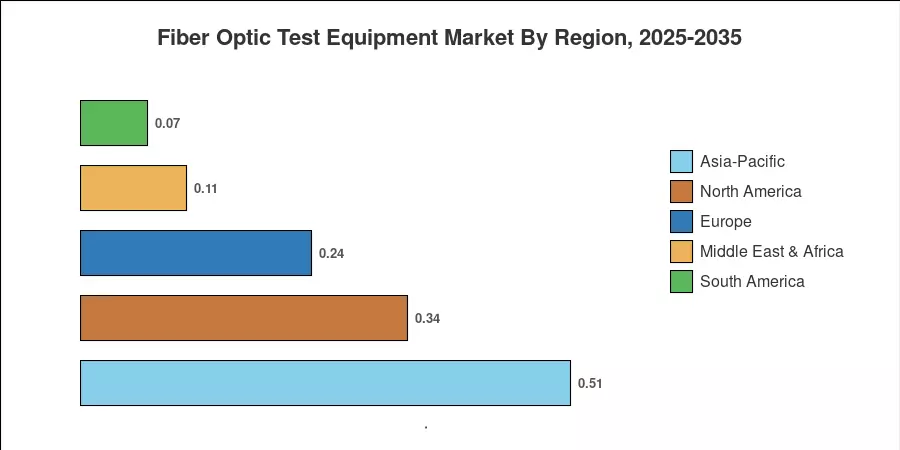

Asia-Pacific is the leader in the fiber optic test equipment market with a share of around 41% of 2025 revenue, driven by China's "East Data, West Computing" infrastructural corridors and India's BharatNet Phase III rollout. The Middle East & Africa is the fastest expanding market with an estimated CAGR of 8.52%, fueled by Gulf-state smart-city fiber build-outs. North America is the second largest, with the federal broadband subsidies and private 5G capex. Vendors that combine hardware precision with software-defined analytics will be rewarded over the next decade.

Key Report Takeaways

• By Equipment Type

- Optical power and loss meters captured 31.20% of the fiber optic test equipment market in 2025, reflecting persistent demand for first-line acceptance testing across telecom and enterprise verticals

- Remote fiber test systems are forecast to grow at an 8.65% CAGR through 2035, the fastest among equipment categories, as utilities and defense agencies adopt continuous monitoring of mission-critical links

- OTDR fiber measurement platforms accounted for approximately USD 0.30 billion in 2025 revenue, anchored by data-center interconnect verification and metro-network expansion

• By End-User Application

- Telecommunications service providers represented 37.10% share of the fiber optic test equipment market in 2025, driven by 5G densification and FTTH last-mile buildouts

- Energy and utilities end users are projected to register a 7.55% CAGR through 2035, propelled by distributed acoustic sensing and smart-grid monitoring requirements

• By Region

- Asia-Pacific retained the dominant position in the fiber optic test equipment market with roughly 41% share in 2025

- Middle East & Africa posts the highest regional CAGR at 8.52% through 2035, fueled by Saudi Arabia's NEOM fiber backbone and UAE smart-city investments

Market Size and Forecast (2021–2035)

The numbers below are from Market Research Future (MRFR). They are based on a proprietary bottom-up model that has been cross-referenced with vendor revenue disclosures, customs trade data for optical instruments (HS 9031.49) and operator capex filings. Historical Values – 2021-2024 Actual Market Performance; 2025 Base Year; 2026-2035 Forecasted Market Values.

.webp?v=1781696924)