Adult Diaper Market Summary

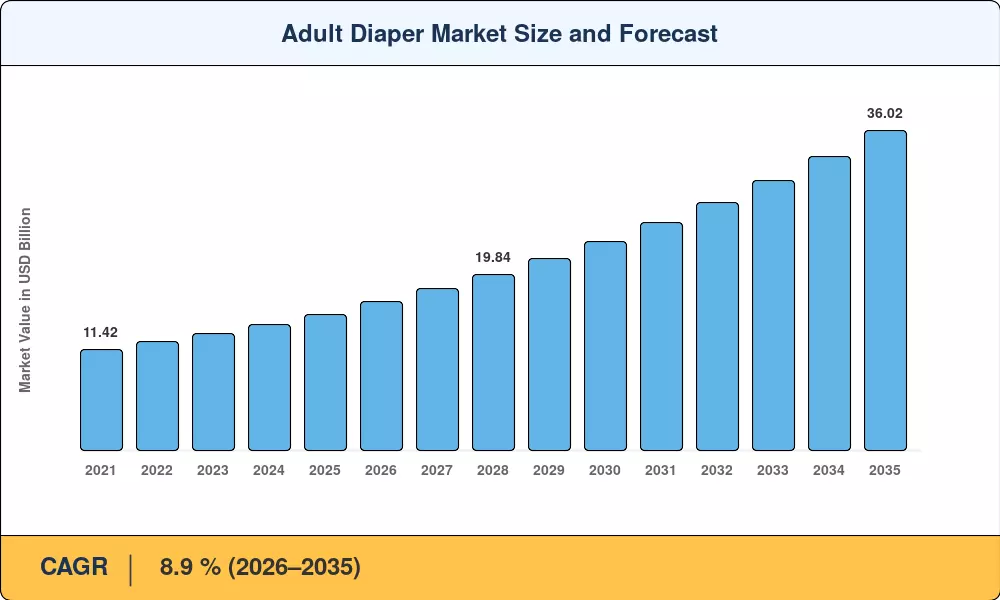

The adult diaper market reached USD 15.36 billion in 2025 and is projected to climb from USD 16.73 billion in 2026 to USD 36.02 billion by 2035, registering a compound annual growth rate of 8.9% across the forecast period. Two macro forces underpin this trajectory: the global population aged 65 and over is expected to double to 1.6 billion by 2050 [1], and public health spending on continence care now exceeds USD 20 billion annually in OECD nations [13]. Government reimbursement reforms — notably the U.S. CMS expansion of durable medical equipment coverage and Japan's Long-Term Care Insurance scheme — are converting latent demand into paid consumption at an accelerating pace [13][14].

Product engineering has shifted decisively from bulky, institutional-grade pads to slim, breathable garments that rival conventional underwear in fit and discretion. Manufacturers invested an estimated USD 1.2 billion in absorbent-core R&D between 2021 and 2024 [6], yielding super-absorbent polymer (SAP) composites that are 40 % thinner yet hold 25 % more fluid than predecessors. Gender-specific sizing and odor-neutralization chemistries have broadened the addressable user base well beyond traditional geriatric applications.

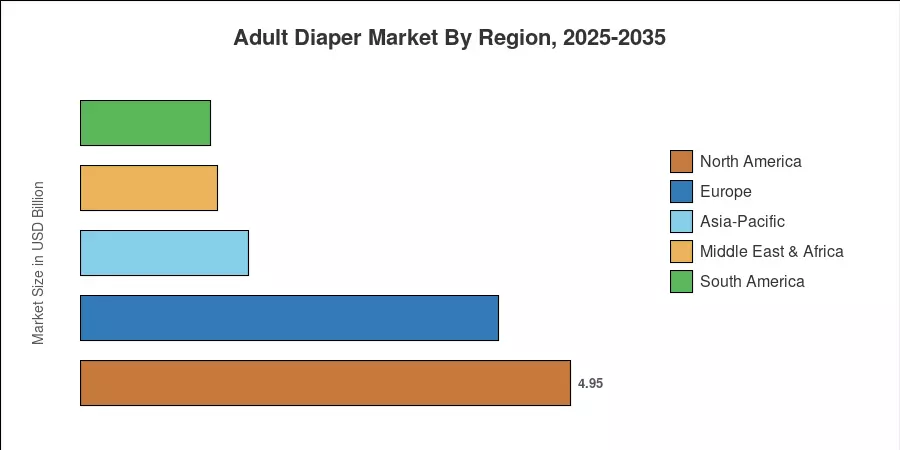

North America commanded roughly 32.2 % of the adult diaper market in 2025, anchored by mature pharmacy distribution networks and widespread insurance coverage. Asia-Pacific is the fastest-growing region at an 11.1 % CAGR, propelled by China's rapidly aging demographics and India's expanding middle-class healthcare awareness. Europe holds the second-largest share at approximately 27.5 %, where Nordic universal-care models sustain high per-capita consumption. As stigma recedes and e-commerce lowers purchasing barriers, the adult diaper market is poised for sustained double-digit regional growth through 2035.

Key Report Takeaways

• By Product Type

- Moderate/heavy diapers accounted for 69.5 % of the adult diaper market in 2025, reflecting sustained demand among post-surgical and elderly users.

- Light diapers are projected to expand at a 10.3 % CAGR through 2035, driven by younger demographics managing mild stress incontinence.

• By Category

- Pads captured 52.1 % revenue share in 2025 due to their cost advantage and ease of use.

- Pant-style (pull-up) products are forecast to grow at 10.5 % CAGR through 2035, favored for active lifestyles.

• By Region

- North America contributed 32.2 % of global revenue in 2025, supported by advanced reimbursement policies.

- Asia-Pacific is recording the highest regional CAGR at 11.1 %, led by demographic shifts in China and India.

- Europe maintained approximately USD 4.22 billion in 2025 revenue, with Nordic countries registering the highest per-capita penetration.

Adult Diaper Market Size and Forecast (2021–2035)

Market Research Future employs a triangulated methodology combining bottom-up revenue models from manufacturer disclosures, top-down cross-validation against national healthcare-expenditure databases, and primary interviews with 120+ supply-chain stakeholders. Historical figures (2021–2024) are reconciled to published company revenues; forecast values (2026–2035) apply the calibrated 8.9 % CAGR with macro-sensitivity adjustments.